Schedule J (1040), Income Averaging for Farmers and Fisherman

Kevin Burkett, Extension Associate, Clemson University

Dr. Steve Richards, Extension Associate, Clemson University

Revised by Mark Dikeman, Executive Director

Kansas Farm Management Association

Department of Agricultural Economics, Kansas State University

Download PDF Version

Watch Webinar

Introduction

Farmers and fishers experience significant variations in income from year to year, which causes their taxable income (and taxes owed) to fluctuate. These fluctuations in income potentially create a higher tax liability overall, due to the progressive nature of the federal income tax code: as income level rises, tax rates also rise (see Table 1). This means that a farmer or fisherman having a good year could end up finding themselves in a higher tax bracket compared to their not-so-good years.

To help these farm businesses smooth out swings in income and reduce overall tax liability, the Internal Revenue Service (IRS) allows individuals engaged in farming or fishing to elect “income averaging” under 26 CFR § 1.1301-1. The definition of farming is found in IRC §263A(e)(4) for this purpose, and is illustrated below. The income which is eligible for averaging includes crop and livestock sales (and fish income) and the sale of personal property used in farming (e.g., machinery and equipment).

Are You a Farmer or a Fisher?

- A farming business is in the trade or business of cultivating land or raising or harvesting any agricultural or horticultural commodity.

- A fishing business is in the trade or business of fishing in which the fish harvested, either in whole or in part, are intended to enter commerce or enter commerce through sale, barter, or trade.

- Aquaculture operations (farm-raised clams, oysters, and fish) are considered farming under the broad definition of “fish” in the IRS definition of farming.

What Are The 2025 Tax Brackets?

The current federal rates are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. The filing status brackets and rates apply equally to each taxpayer regardless of their industry. These percentages have changed over time due to tax law changes and inflation adjustments, but Table 1 below illustrates where they presently stand in 2025.

Table 1. 2025 Married Filing Jointly Income Tax Rates and Taxable Income Brackets

|

Tax rate |

on taxable income from . . . |

up to . . . |

|

10% |

$0 |

$23,850 |

|

12% |

$23,851 |

$96,950 |

|

22% |

$96,951 |

$206,700 |

|

24% |

$206,701 |

$394,600 |

|

32% |

$394,601 |

$501,050 |

|

35% |

$501,051 |

$751,600 |

|

37% |

$751,601 |

And up |

Example 1: An Example of Tax Brackets and Progressive Taxation

A taxpayer earning $126,950 in taxable income would be in the marginal 22% bracket and owe $17,757 in taxes. How the tax is calculated is shown below. Notice how each “bracket” in income is taxed at a higher rate as income rises.

- The 10% rate is applied on income up to $23,850 (10% x $23,850 = $2,385)

- The 12% rate is applied for income between $23,851 and $96,950 ($96,950 - $23,851 = $73,099. $71,099 x 12% = $8,772)

- The 22% rate is applied for income between $96,951 and $126,950 ($126,950-$96,951 = $29,999. $29,999 x 22% = $6,660)

- Total taxes owed in this example: $2,385 + $8,772 + $6,660 = $17,757

Using Income Averaging

One of the first steps in tax planning is figuring out which tax bracket a taxpayer typically falls into. With income averaging, a taxpayer can “move” income from the current year (known as Elected Farm Income, even if you are a fisher) and move it to prior years (base years) under prior years’ tax rates (see Figure 1).

This effectively allows the taxpayer to “fill up” unused brackets of the prior years. The benefit would be that income taxed at a higher rate for the current year can be taxed at lower rates due to the taxpayer’s lower income level and tax brackets experienced in previous years.

Example 2: Income Averaging

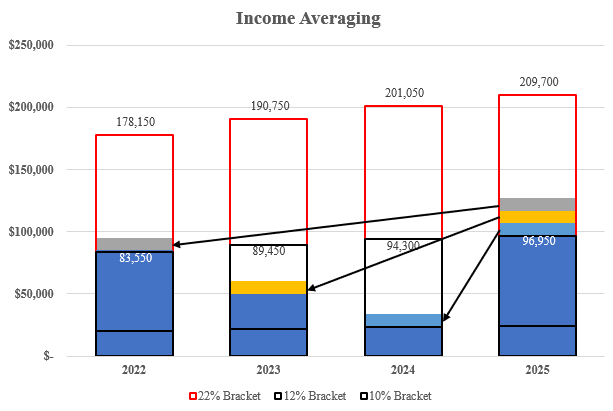

Figure 1 illustrates a farmer or fisher who experiences a taxable income jump in 2025, with an income of $126,950. The three prior years (2022 to 2024) were not as good as 2025, leading the producer’s accountant to suggest income averaging. Some details of this example:

- 2025 is the Elected Farm Income year, and the base years are 2022, 2023, and 2024.

- The taxpayer elects $30,000 from 2025 to average with 2022, 2023, and 2024 tax years. Per income averaging rules, the elected income must be divided equally among the three prior years (equaling $10,000 per year).

- The marginal tax brackets in prior years were 2022 at 22%, 2023 at 12%, and 2024 at 12%. By applying $10,000 to these prior tax year brackets, the taxpayer can apply a 12% tax rate to $20,000 (2023 and 2024) and pay the same tax rate on the $10,000 applied to 2022 (the 22% tax bracket, the same as 2025).

- This means with the income averaging election, the taxpayer saves around $2,000 by applying 12% to the $20,000, instead of the originally calculated 22% rate.

Figure 1: Illustration of How Income Averaging Works to Help Reduce Overall Taxes

Tax Planning

For the current year, the income averaging benefit is maximized when the rates from averaging are the same as the current year rate. For instance, if the averaging rate is 22% for each of the base years (past three years) and the current year rate is 22%, there is no further tax benefit. Once income averaging has been applied, it does affect future income averaging calculations. In Figure 1, the $30,000 that has been moved from 2025 to the prior three years will be part of any future calculations. Continuing the example, in 2026 if income averaging were to be elected again, the $10,000 (each) that was moved to 2022, 2023, and 2024 would still apply. 2022 would no longer be part of the calculation (only the prior 3 years are used), so 2023, 2024, and 2025 would be the base years. If 2026 income levels were also in the 22% bracket, it may be another opportunity for the taxpayer to income average as there are still “gaps” in the 2023 and 2024 tax years’ 12% brackets. Sometimes, if a taxpayer or preparer anticipates a higher income year is coming, they may income average with no current year benefit, so when they make the calculation in future years, they have created bigger bracket “gaps” for future years to fill.

Other Considerations

The examples in this article are for educational purposes and illustrate the concept and benefits behind income averaging. Only individuals can utilize this provision, meaning that estates, trusts, and C Corporations are not eligible. For those in a partnership, S Corp, or LLC, their share of farming or fishing income is averaged on their Form 1040, U.S. Individual Income Tax Return. If an individual was involved in both a farming and fishing operation, those incomes are combined for the purposes of Schedule J (Form 1040), Income Averaging for Farmers and Fishermen. Certain items of income are includable (sale of business assets for instance) and other items are excludable (sale of land). For these reasons, we encourage you to work with your trusted tax professional to understand the impact of Schedule J (Form 1040), Income Averaging for Farmers and Fishermen for your operation.

IRS Publications

For more information on or to access Schedule J (Form 1040), Income Averaging for Farmers and Fishermen; IRS Publication 225, Farmer's Tax Guide; or other forms and publications, visit the IRS website at www.irs.gov. Type the form, schedule, or publication number or title in the search box.Additional Topics

This fact sheet was written as part of Rural Tax Education, a national effort including Cooperative Extension programs at participating land-grant universities to provide income tax education materials to farmers, ranchers, and other agricultural producers. For a list of universities involved, other fact sheets, and additional information related to agricultural income tax, please see RuralTax.org.

This information is intended for educational purposes only. You are encouraged to seek the advice of your tax or legal advisor, or other authoritative sources, regarding the application of these general tax principles to your individual circumstances. Pursuant to Treasury Department (IRS) Circular 230 Regulations, any federal tax advice contained here is not intended or written to be used, and may not be used, for the purpose of avoiding tax-related penalties or promoting, marketing or recommending to another party any tax-related matters addressed herein.

USDA is an equal opportunity provider, employer, and lender. Rural Tax Education is part of the National Farm Income Tax Extension Committee. The land-grant universities involved in Rural Tax Education are affirmative action/equal opportunity institutions.

This material is based upon work supported by the U.S. Department of Agriculture, under agreement number FSA21CPT0012032. Any opinions, findings, conclusions, or recommendations expressed in this publication are those of the author(s) and do not necessarily reflect the views of the U.S. Department of Agriculture. In addition, any reference to specific brands or types of products or services does not constitute or imply an endorsement by the U.S. Department of Agriculture for those products or services.

Revised August 2025

Back to Top